The ruble is too strong - really

The ruble is too strong - really

Russian exporters need a weaker real exchange rate. Some devaluation is coming. The Russian Central Bank will not like it.

The ruble exchange rate is a double-edged sword for Russia. A strong ruble has many benefits: It means more purchasing power for Russian consumers and businesses when importing goods and services from abroad. Particularly in times of sanctions, when importing often involves extra costs due to complicated payment and logistics schemes, a strong ruble can mitigate some of this. By keeping Russian imports cheap, a strong ruble has a dampening effect on inflation.

A strong ruble makes life difficult for exporters because their costs, such as salaries, are in rubles and their revenues are not. A strong ruble reduces their profits. Local producers also suffer when they have to compete with cheaper imports. The same goes for Russian budget revenues, which siphon off most of the high margins of Russian oil producers. When the ruble is strong, tax revenues shrink.

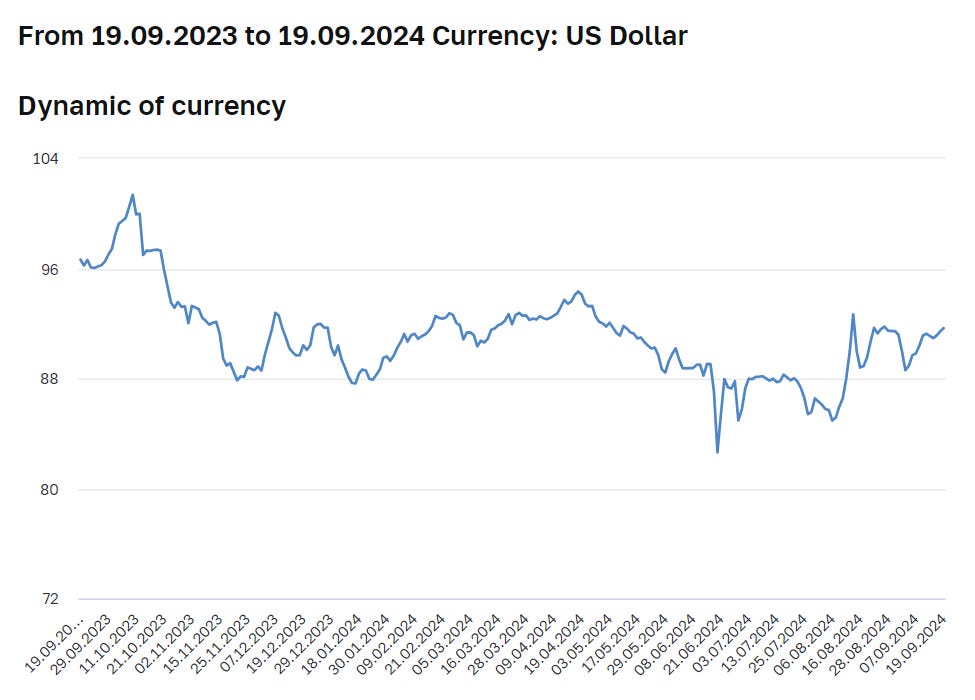

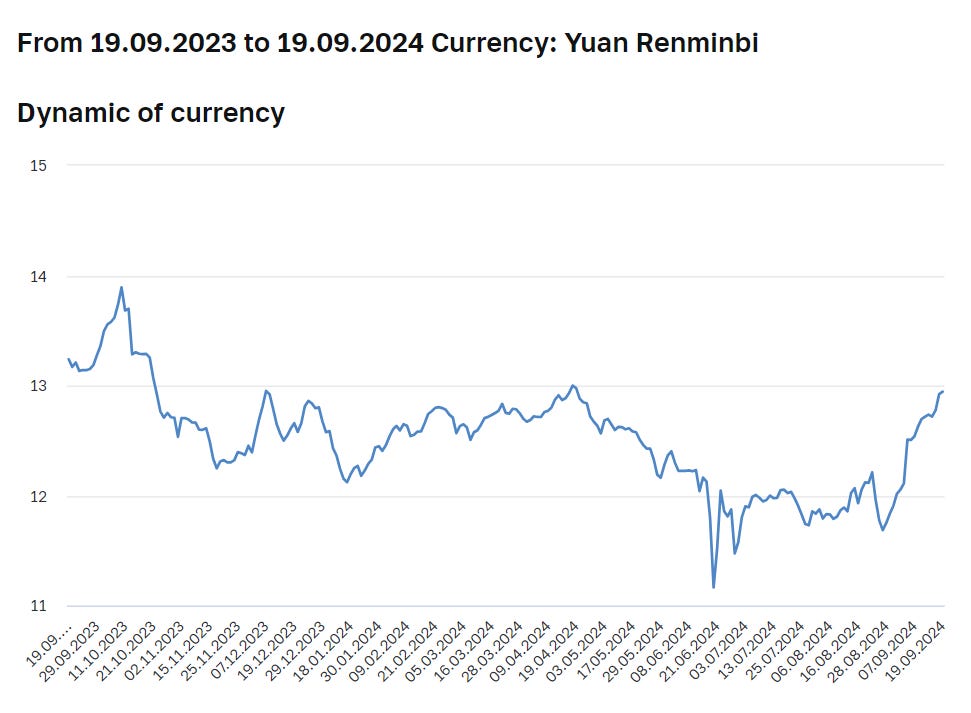

Some observers of the Russian economy may wonder: “But wait! The ruble exchange rate has barely changed from a year ago.” But that is precisely the point. Consider that Russia’s inflation rate in August 2024 was 9.1%. If the ruble doesn’t change in nominal terms despite inflation, that means it’s strengthening in real terms.

It may not be intuitive to think that inflation makes a currency stronger in real terms. It helps to think not about what a single ruble buys in the world, but what an average Russian salary buys in the world. If Russian salaries go up because of inflation, but the exchange rate doesn’t move, that means salaries have gone up in dollar terms.

Image: Exchange rates of Russian ruble vs. US dollar and Chinese renminbi. Source: Russian Central Bank.

This effects of the real exchange rate appreciation can already be seen in the profit margins of Russian exporters: The strong ruble is part of the problem for Russian coal exporters. Some Russian manufacturers are also suffering. Because nominal wages are rising in Russia, but Chinese cars - priced in rubles - don’t increase in price, Russian carmakers such as Avtovaz/Lada (who have to pay Russian wages) find it hard to compete. This is why Russia is significantly increasing trade barriers (the so-called utilization fee - a tariff in all but name) for Chinese cars in order to protect Lada’s market share in Russia.

The real ruble appreciation also means that Russia’s budget revenues from oil and gas remain flat, while Russian budget expenditures, such as pensions, rise with inflation. As a result, oil and gas can finance a smaller share of budget spending, and non-oil/gas taxes or borrowing must make up the difference. In contrast, last year’s depreciation of the ruble helped Russia’s finance ministry to avoid a larger deficit.

However, there is one big fan of the strong ruble: The Russian Central Bank. Without today’s real ruble strength, Russia’s inflation problem would be worse.1 While some are shaking their heads at the latest increase in key interest rates, this may be the Central Bank expecting a weakening of the ruble, which will be inflationary.

For the Russian budget, a devaluation of the ruble would have ambiguous effects. As mentioned above, it is initially beneficial because it increases tax revenues. However, as the weaker ruble leads to higher inflation, it will later mean higher pension indexation and wage increases for state employees.

The effect of inflation on Russia’s budget balance has become less positive due to the war: At a time when the Russian state is hiring new employees (soldiers) like never before, the share of budget spending that rises with inflation also increases. In the long run, there is a sweet spot in this inflation trade-off of “more revenues” and “more spending”. Russian economist Dmitri Nekrasov described this sweet spot as ruble devaluation that is slightly above the inflation rate in a recent analysis for iStories. This would bring the ruble-dollar exchange rate firmly above 100, or 10-20% weaker than today’s rate.

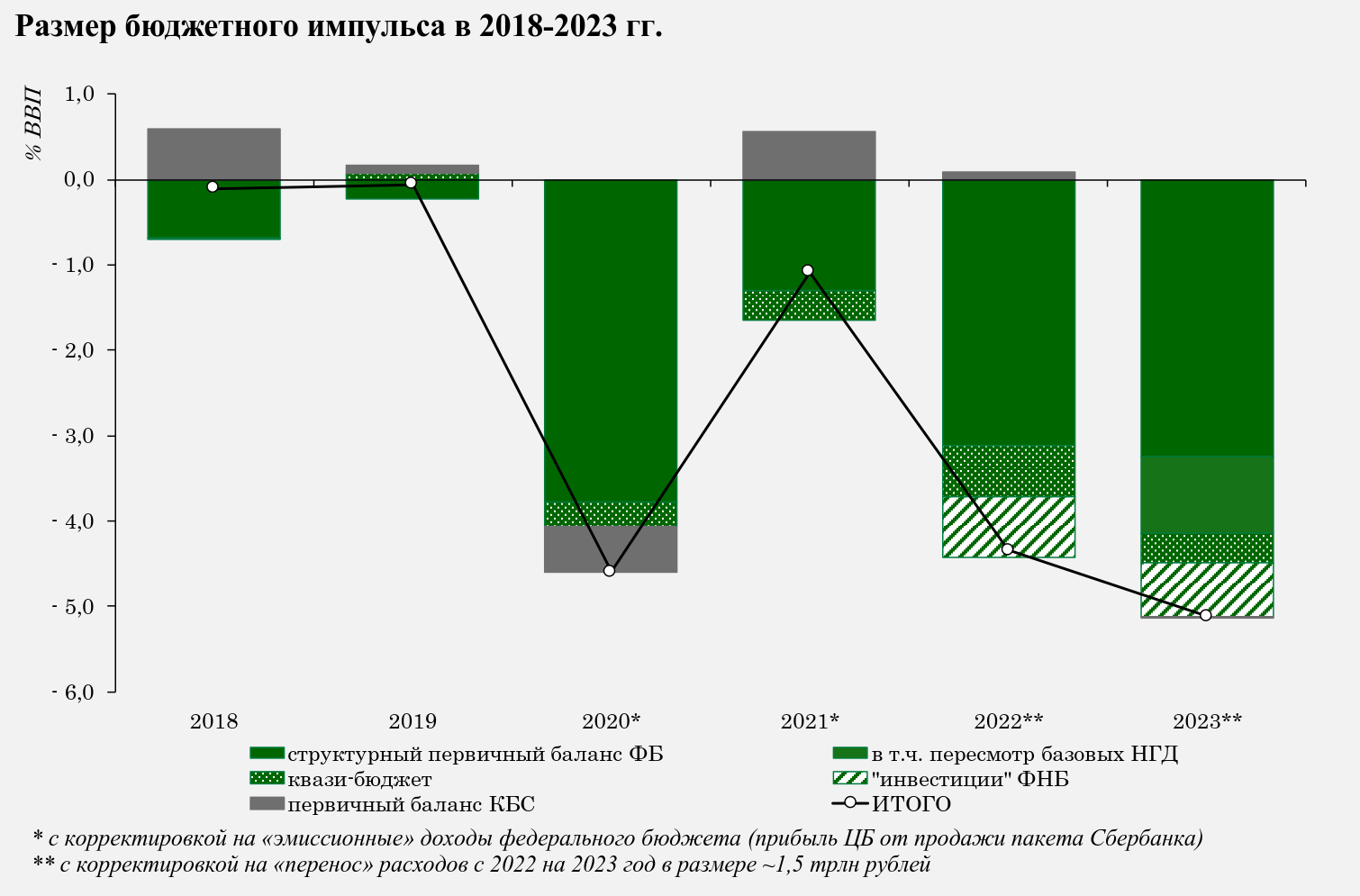

But why is the ruble so strong in real terms? If you are up for some economics fun, here we go: There are several external factors at play, such as oil prices, remaining capital controls, and sanctions restrictions on Russia’s ability to import.2 But a key reason is Russia’s spending on the war: Real exchange rate appreciation is often the result of a strong fiscal impulse. Russia’s Finance Ministry has estimated that the war led to a fiscal impulse of 5% of GDP in both 2022 and 2023.

Image: Size of fiscal impulse 2018-2023. Source: Russian Finance Ministry.

The impact of a fiscal impulse on the real exchange rate depends (among other things) on its effect on imports. Can the additional demand created by the government be met by an increase in imports? This would tend to weaken the ruble. Or will most of the demand be for goods and services that can only be produced in Russia, requiring more intensive use of Russian capacity? Russia’s war spending falls firmly into the second category, i.e. it has a strengthening effect on the real exchange rate.

For example, when the Russian army recruits for war, it creates strong demand for a particular service (fighting in Ukraine) that can only be "made in Russia," leading to rising wages for Russian labor, inflation, and consequently real exchange rate appreciation (because the trade balance is not initially affected).

If the Russian government consumes lots of weapons (or “invests in weapons”3) with a specialized Russian supply chain, this means that the increase in demand has to be met with Russian capacities, and increasing imports cannot help much (imports from Iran and North Korea are only a small fraction of Russian weapons demand). Strong state demand for weapons can only affect Russia’s trade balance indirectly in the form of lower metals exports, because metals are needed in the Russian military industry, or maybe imports of other basic materials such as nitrocellulose, and possibly lower arms exports (which, however, were always rather small in comparison to total Russian arms production). But these effects on the trade balance are relatively small.

Therefore, the additional demand created by Russia’s war spending does not initially weaken the ruble. It creates a special kind of demand for goods and services "made in Russia", but not for goods and services produced abroad. The result is rising ruble wages and ruble prices for Russian-made goods, while ruble prices for foreign-made goods remain unchanged - the very definition of real exchange rate appreciation.

While it may seem that way, there is no vicious circle here. To some extent, a weaker ruble leads to higher inflation, which in turn can lead to further weakening of the ruble. But the second-round effect is only a fraction of the first-round effect, and the third-round effect is even smaller, and so on. While there is a certain “multiplier” to take into account when estimating the effect of a weaker ruble on inflation, it is not a downward spiral.

If an economy is integrated into global capital markets, a strong currency could be part of the exchange rate channel of monetary policy at work: Higher interest rates (as in Russia now) would attract foreign capital or bring home domestic capital, strengthening the currency and slowing inflation. However, Russia's links to global capital are largely severed by sanctions, so high interest rates do not attract more capital to Russia.

When the government buys a tank, it is statistically treated as investment. High investment rates have led some observers to marvel at the Russian investment miracle, even though “investing in tanks” does nothing for Russia’s productivity or long-term growth prospects.