Russian federal budget spending in Q1/2025

In the first quarter of 2025, classified spending increased significantly, indicating further militarization of the Russian federal budget.

Russia is in the process of amending its federal budget law for 2025 and the outlook for 2026/2027. Mainly due to lower-than-expected oil/gas revenues, the expected deficit will increase from 0.5% of GDP to 1.7% of GDP this year.

Yesterday, the Russian government introduced the amendments law into the State Duma. One of the documents attached to the project provides an overview of budget spending in the first quarter of this year. Given that we don’t even have Q4/2024 data yet, this is a welcome look at the latest data. Keep in mind that this only covers open (unclassified) spending. This is especially important for the defense budget, which is over 80% classified. However, classified spending can be calculated by comparing open spending to total spending, which is also published by the Finance Ministry.

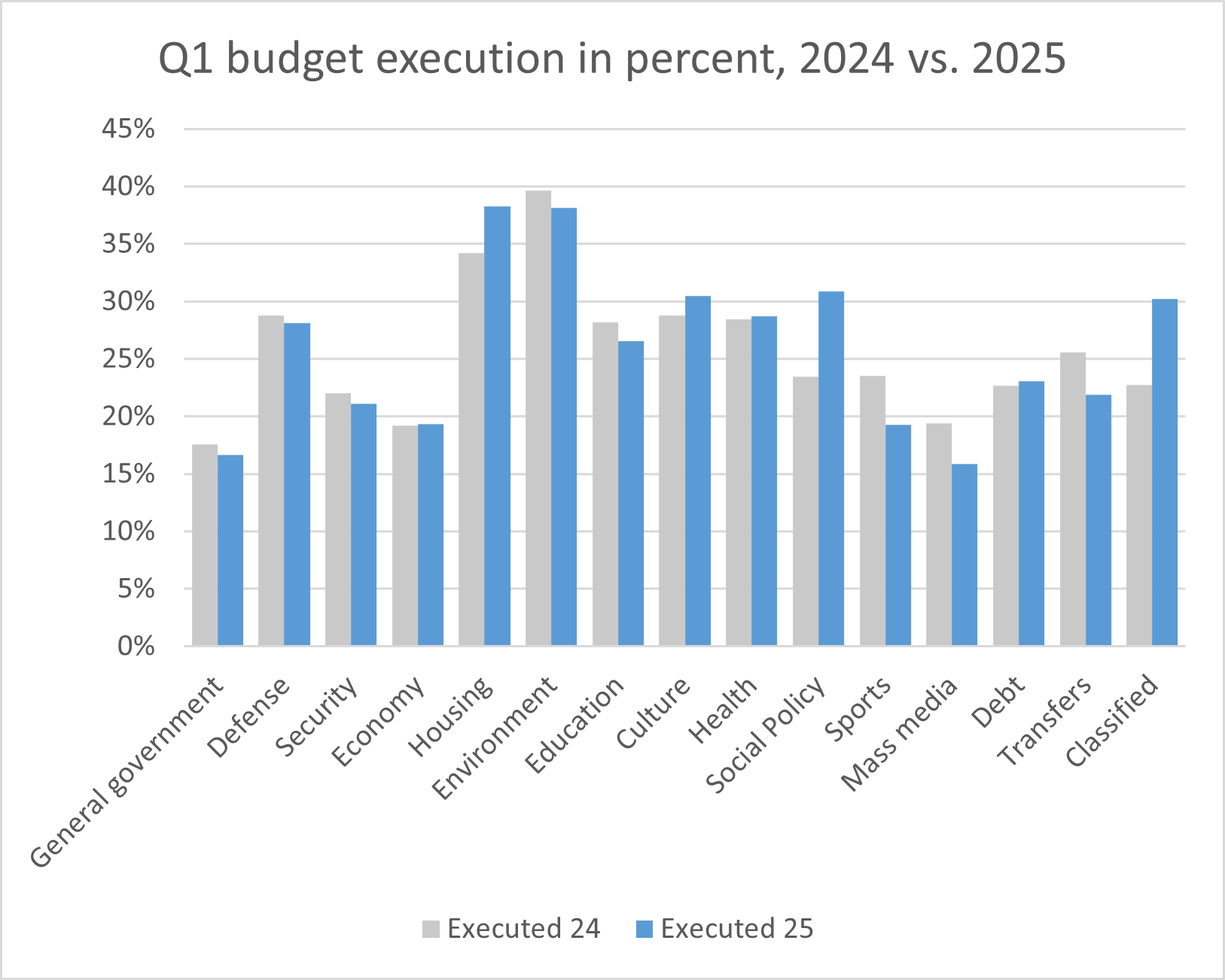

The pace of budget spending varies from quarter to quarter. To identify unusual spending patterns, it is helpful to compare Q1/2025 spending to Q1/2024 spending. The following chart shows the level of budget execution as a percentage of the planned budget for that year.

While the overall execution is not much different from last year, there are three notable changes:

The first is housing, where 38.3 percent of planned spending has already been executed. While this chapter also includes subsidies for construction in the annexed territories, the unexpected increase in spending is caused by something else: Higher interest rates. Until last summer, the Russian government offered subsidized mortgages, mostly at an interest rate of 8%. Most of these subsidies programs have since been ended, but the existing stock of subsidised loans causes costs that depend on the interest rate: Since the budget has to compensate the banks for the delta between the market rate and the subsidized rate, the high key rate of the Central Bank of Russia leads to increased spending.

The second is social policy, where 30.9% of the allocated funds were spent in Q1. Social policy spending for 2025 has been reduced in nominal terms compared to 2024, as transfers to the pension systems are expected to decline. The improved balance of the pension system is a result of the 2018 pension reform (raising the retirement age) and very low unemployment. For 2024, the planned support for the pension system from the federal budget was about 4 trillion rubles, this year it is only 2.4 trillion rubles. However, in the first quarter of 2025, transfers to the pension system were actually slightly higher than last year (584 billion instead of 520 billion). Sometimes there are unplanned transfers to the pension system, which may explain this. Of course, slower wage growth, high inflation and higher unemployment would also mean that the pension system would need additional subsidies, so there are budgetary risks here for the rest of the year. However, the slight slowdown in the economy in the first quarter is unlikely to have caused higher spending here, so a question mark remains.

The third notable increase is in classified spending. Classified spending is calculated as the difference of total spending (published by the Finance Ministry) and open spending. Last year, classified spending in the first quarter was 2.5 trillion rubles, this year it is 3.6 trillion rubles. This is most likely due to spending on arms procurement. In its commentary on the budget spending in the first months, the Finance Ministry mentioned advance payments for procurement as a driver of more spending in the early months this year.

Last year Russia spent a total of 9 trillion rubles in the first quarter, this year it was 11.2 trillion rubles. About half of the increase is due to (mostly military-related) classified spending. Taking into account that open defense spending also increased, this shows that further militarization of the budget was the main driver of higher spending. However, the impact of higher interest rates (on housing, but also on debt servicing costs) is also affecting Russia's budget balance.

For a comprehensive analysis of Russia’s federal budget and military spending in 2025, I recommend the latest SIPRI paper by Julian Cooper.